Whether you’re mid-career or nearing retirement, it’s important to know where you’re investing — and how those accounts could impact future taxes, experts say.

Many workers are heavily concentrated in tax-deferred savings via a pretax 401(k) plan or traditional individual retirement accounts, which incur regular income taxes on future withdrawals, based on federal tax brackets.

However, many advisors recommend using a mix of pretax, after-tax Roth and taxable brokerage accounts for more flexibility in retirement.

The right mix can provide “a lot of different levers to pull to manage your adjusted gross income,” explained certified financial planner Judy Brown at SC&H Group in the Washington, D.C., and Baltimore area.

More from Personal Finance:

I lost my wallet. Here’s what experts say I should do to protect my identity and money

Weddings cost over $30,000: Couples are having ‘micro weddings’ instead

This ‘bucket strategy’ could lower your taxes in retirement — how to maximize it

Pretax distributions could bump you into a higher tax bracket or trigger higher Medicare Part B and Part D premiums, explained Brown, who is also a certified public accountant.

Medicare Part B and Part D premiums are based on so-called modified adjusted gross income, which is your adjusted gross income plus tax-exempt interest, from two years prior.

By comparison, after-tax account distributions, such as Roth 401(k) plans or Roth IRAs, generally don’t incur levies and won’t boost your earnings.

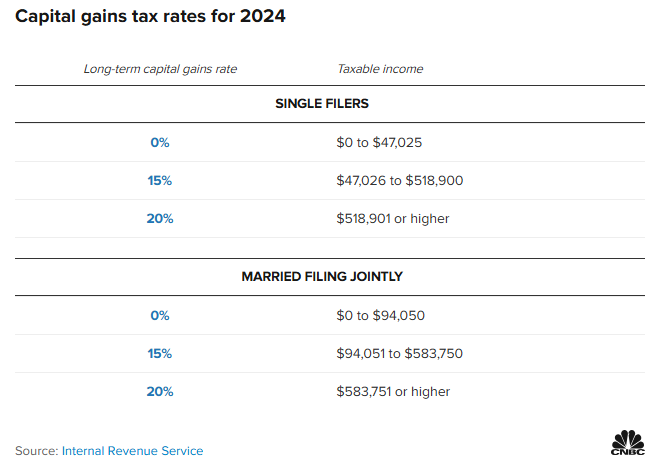

Another bucket is taxable brokerage investments. If you hold these assets for more than one year, you’ll pay 0%, 15% or 20% on capital gains, depending on your taxable income.

While higher earners could incur an extra 3.8% levy on brokerage assets, the combined rate is still considerably lower than the 37% top marginal tax rate on pretax account distributions.

A mix of pretax, after-tax Roth and taxable assets can help you “adapt to changing tax laws and personal financial circumstances” to better manage withdrawals and taxes, said CFP Alyson Basso, managing principal of Hayden Wealth Management in Middleton, Massachusetts.

The perks of a brokerage account

Your brokerage assets can be especially useful if you’re eyeing an early retirement before age 59½, according to Houston-based CFP Abrin Berkemeyer with Goodman Financial.

Workplace retirement plans and pretax IRAs typically incur a 10% penalty for withdrawals before age 59½, with some exceptions. However, you can tap your brokerage account at any age without penalty.

The brokerage account can also help you achieve other goals before age 59½, such as covering a down payment on a second home orfunding a child’s wedding, Berkemeyer said.

Of course, you’ll sacrifice certain tax benefits to build your brokerage account, such as tax-free growth or upfront deductions for contributions, he said.

But ultimately, the right mix of pretax, Roth and taxable investments depends on your goals, risk tolerance and timeline.