Some 401(k) plans allow after-tax contributions, letting you bypass the $20,500 annual deferral limit if you’re under 50 for 2022.

If you can afford to max out your 401(k) and there’s still wiggle room in your budget, your plan may have a special feature to save even more.

Although the 401(k) deferral limit for 2022 is $20,500 if you’re under 50, you can use after-tax contributions to save up to $61,000, including employer matches, profit sharing and other plan deposits.

And you can use the funds for the so-called mega-backdoor Roth maneuver — paying levies on earnings and moving the money to a Roth individual retirement account — for future tax-free growth.

An estimated 12% of employees maxed out 401(k) plans in 2020, according to Vanguard, and 10% of workers with access to after-tax 401(k) contributions participated.

“It can be a really really powerful technique for the right individual,” said certified financial planner Dan Galli, owner at Daniel J. Galli & Associates in Norwell, Massachusetts.

By rolling the money into a Roth IRA, investors may start building a tax-free pot of money for retirement, without rules to take the money out at a certain age.

“If they’re young enough and have years of tax-free growth ahead of them, it could be a game-changer,” said JoAnn May, a CFP and CPA with Forest Asset Management in Berwyn, Illinois.

After-tax vs. Roth 401(k)

It’s easy to confuse after-tax 401(k) contributions with a Roth 401(k) account since both allow you to save money after taxes, but there are key differences.

For 2022, employees under age 50 may defer up to $20,500 of their salary into their company’s regular pretax or Roth (after-tax) 401(k) account.

However, you can make additional after-tax contributions to your traditional 401(k), which allows you to save more than the $20,500 cap.

For example, if you defer $20,500 and your employer kicks in $8,000 for matches and profit-sharing, you may save another $32,500 before hitting the $61,000 plan limit for 2022.

The other twist is how earnings are taxed. While Roth 401(k) withdrawals (including earnings growth) are tax-free in retirement, any earnings on those “bonus” amounts added to traditional 401(k) plans are taxed. Yes, it’s confusing.

“That’s why it’s important to get [after-tax contributions] out of the 401(k) plan periodically,” said May.

Once per year, her clients withdraw after-tax contributions and earnings and roll the money into a pretax or Roth IRA. The downside of the Roth IRA option is there may be a tax bill on growth at the conversion.

Keep in mind the feature isn’t available for all plans.

While many 401(k) plans offer Roth accounts, after-tax contributions are less common. Fewer than 20% of 401(k) plans provided after-tax contributions in 2020, Vanguard reported.

Moreover, plans with after-tax 401(k) contributions may not educate employees about the option. In some cases, advisors may discover the feature buried deep within a client’s benefits paperwork.

“The most important thing is to read your employee benefits handbook and pass it on to your advisor,” said May.

Tax-free retirement income

Whether someone leverages after-tax or Roth contributions, tax-free money may be valuable in retirement, said Galli.

When clients apply for Social Security, their portfolio income may hurt those benefits. Retirees may pay income taxes on up to 50% to 85% of their Social Security payments, depending on their modified adjusted gross income.

About 40% of those who receive Social Security income pay taxes on their benefits, according to the Social Security Administration.

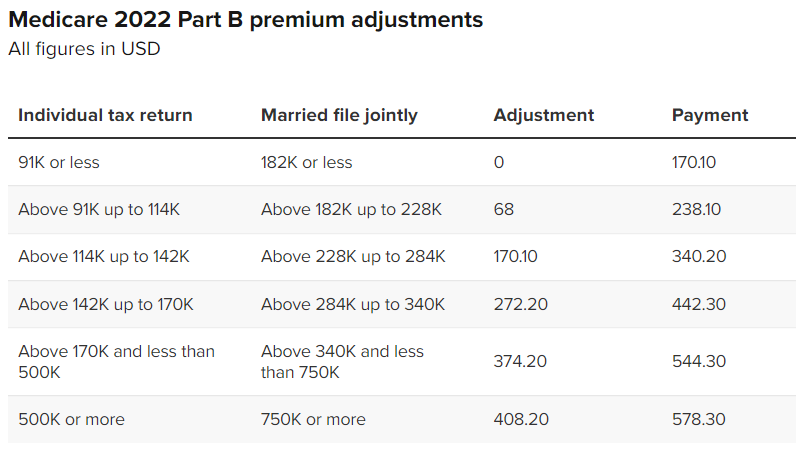

Some retirees may also pay more for Medicare premiums. While most retirees don’t pay for Medicare Part A, the base price for Medicare Part B starts at $170.10 for 2022.

Depending on their income, retirees may have to pay more for Medicare Part B, with top earners paying monthly premiums of $578.30.