People engaged in frequent sales of real property need to determine whether they are real estate dealers or investors. The distinction is important because dealers and investors are treated very differently for tax purposes.

Tax Consequences of Dealer vs. Investor Status

Real estate dealers buy and sell properties as part of their regular business operations, with profits taxed as ordinary income and subject to self-employment tax.

Real estate investors purchase and hold properties primarily for long-term appreciation or rental income, typically enjoying favorable tax treatment such as capital gains rates and depreciation benefits.

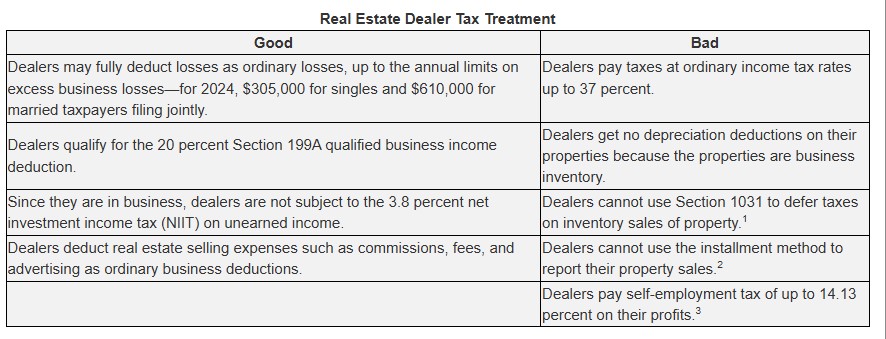

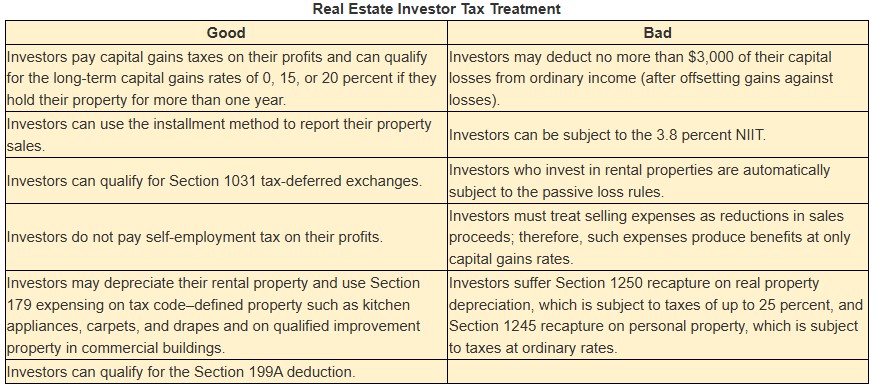

Dealers and investors receive very different tax treatment, as shown in the following overview charts. Note that there are good and bad elements to each tax classification, but being classified as a dealer is usually not advantageous taxwise.

Since dealers pay tax on their profits at ordinary income rates (plus self-employment tax), while investors pay tax at capital gains rates, dealer status is particularly undesirable where real property is sold for a substantial gain.

Example. You earn a $100,000 profit from the sale of a property held for more than one year. If you are a dealer with income from other sources, your taxes could be as high as $51,130 (37 percent income tax + 14.13 percent self-employment tax). If you’re an investor, your taxes could be as high as $23,800 (20 percent capital gains tax + 3.8 percent NIIT). That’s a $27,330 difference ($51,130 – $23,800).

“Real Estate Dealer” Defined

A real estate dealer is someone who is in the business of owning property primarily for sale to customers. Real estate dealers resemble merchants or retailers of goods, except that their product is real estate. A real estate dealer’s holdings are inventory for sale to customers, the same as any merchant’s inventory.

Real estate dealers typically include (but are not limited to)

- real estate flippers—people who buy homes, fix them up, and resell them quickly;

- real estate speculators, who buy and sell many properties each year;

- subdividers, who buy large tracts of vacant land, divide the tracts into smaller lots, and then resell the lots piecemeal; and

- real estate developers and home builders, who construct new houses and resell them soon after completio

There is no definition of “real estate dealer” in the tax code. The IRS and courts look at the following eight factors. No single factor is determinative, but the first three are the most important.

1. The number and frequency of sales. The number and frequency of sales are the most important factors. Frequent and substantial sales are the hallmark of a real estate dealer. On the other hand, infrequent sales for significant profits indicate that an investor held the real property as an investment.

There is no set number of sales required to make a person a dealer. As the following chart shows, courts have been inconsistent in deciding how many sales are needed to be a dealer.

2. Intent in buying property. A real estate dealer buys properties with the intent of making money from reselling them. A person who buys property to earn income and/or benefit from long-term appreciation is not a dealer. A dealer is in the business of buying and selling properties.

3. Extent of improvements. Dealers often improve the property they own to increase its value for purposes of resale.14 Thus, for example, a person who frequently “flips” property would likely be a dealer.

4. Sales efforts. Dealers make extensive efforts to resell their properties—for example, they hire real estate brokers, list their properties for sale, engage in advertising, and may have their own sales office and sales staff. A person who engages in extensive marketing efforts is more likely a dealer than one who takes a passive sales approach.

5. How the property is acquired. Dealers go out and buy properties themselves. A person who acquires real property through an inheritance or gift is not likely to be viewed as a dealer.

6. Holding period. Like any merchant, real estate dealers want to sell their inventory quickly. People who hold real property for a long time before selling it are much less likely to be considered dealers than those who hold their properties for a short time.

7. Income generated by sales. A person is more likely to be viewed as a dealer if the income generated from selling real estate constitutes a substantial amount of the total income he or she earns.

8. Continuous effort. Dealers work continuously throughout the year to sell their properties and spend substantial time at their business. A person whose sales transactions are only intermittent is not likely to be a dealer.

“Real Estate Investor” Defined

Real estate investors own property primarily to earn income from rents and/or long-term appreciation.

Unlike dealers, they sell their property infrequently, usually after a long holding period. But there is no prescribed minimum holding period to qualify for investor status.

Real estate held for a long time and appreciating in value with minimal improvements is likely to be deemed an investment.

Investors can fix up their property, but they do so primarily to increase its rental value, not to earn more profits on a quick sale.

You will generally be deemed an investor if you acquire property though inheritance or through foreclosure of a mortgage.

You Can Be Both a Dealer and an Investor

Whether you are a dealer is determined on a property-by-property basis. You can own some property for sale as a dealer and other property as a long-term investment.

Example. Peter Miller, a real estate broker, purchased an apartment building and sold it two years later for a substantial profit. At the same time, he worked as a dealer in real estate: he was involved in several real estate sales businesses, including subdividing land for resale and home building. Nevertheless, the Tax Court found that the apartment building was not dealer property. Miller owned the apartment building primarily to earn rental income, not for resale purposes.

But if you are a real estate dealer, all the property you own can be subject to “dealer taint” and classified as dealer property. You should take the following steps to overcome such taint:

Keep separate books, records, and bank accounts for your investment and dealer properties.

- If possible, establish a separate business entity, such as a single-member limited liability company (LLC), for your investment properties,. The name of the entity should not include the words “development” or “developers” but should include “investments” or “investors.” The entity’s governing documents should state that the entity’s purpose is investment. Tax returns filed by such an entity should list “investment,” not “development,” as its principal activity.

- Document your investment intent with resolutions, minutes, and similar paperwork.

- Never deduct your expenses for your investment property as business expenses; deduct them only as investment expenses (e.g., on Schedule E for rentals).Keep track of the time you spend on your dealer properties versus your investment properties. Your investments should take up much less of your time.

- Use third-party brokers or agents when you sell your investment property, rather than selling it yourself.

Dealer Property Can Become Investment Property and Vice Versa

The fact that a piece of property was dealer property when acquired doesn’t necessarily mean it must still be dealer property when sold. You may initially purchase property for sale to customers but later decide to hold it for investment, transforming it into investment property.

In one case, for example, an LLC purchased land with the intent to subdivide and develop it but was unable to do so due to the subprime mortgage crisis. It decided to hold the land for investment and sell it once the market improved.

The LLC members’ decision to convert the land to investment property was well documented in a unanimous LLC member resolution. The LLC never solicited purchasers but ultimately sold the unsubdivided land when approached by an interested buyer. The Tax Court held that the property was investment property when sold.

On the other hand, property initially acquired as an investment may become dealer property at the time of sale if the owner’s intent changes—that is, a taxpayer may decide to develop and sell property initially purchased and held for investment.

Takeaways

Here are five takeaways from this article: